“In an AI-native world, the question isn’t just how financial products are distributed – but what distribution even means when every product, price, or service is just a prompt away.”

Despite decades of technological change, core financial products remain largely the same. A checking account is still a deposit. A mortgage is still a secured loan. A credit card is still a revolving line of credit.

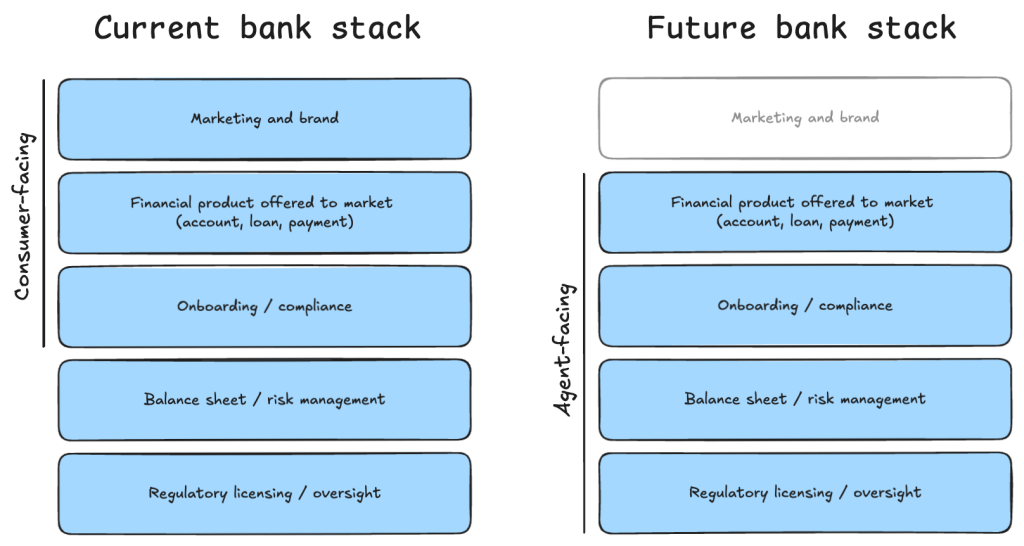

What has changed is distribution.

The most successful fintech companies didn’t create new financial products – they made existing ones easier to access through new interfaces. Visa scaled credit via telecom rails. PayPal brought payments to the early web. Square turned smartphones into point-of-sale systems for small businesses. Robinhood unlocked retail investing by building a mobile-first brokerage with zero-friction onboarding. Stripe gave developers instant access to payments with a few lines of code.

Each of these companies aligned with the dominant distribution platform of their era – telecom, web, or mobile – and built around it. Their edge wasn’t product innovation. It was distribution design.

That brings us to today. In an AI-native world, the question isn’t just how financial products are distributed – but what distribution even means when every product, price, or service is just a prompt away.

AI and the End of Front-End Finance

AI changes the shape of distribution – not by adding another interface, but by removing the need for one.

Where previous technologies required a user to browse, compare, or engage with an application, AI allows users to delegate those steps entirely. You ask for a mortgage, and the system compares rates, accounts for fees and closing costs, and executes. There’s no scroll, no search, and no form.

This fundamentally alters how products are selected. The user doesn’t make the choice – the agent does. The agent doesn’t care about brand – it evaluates structured inputs: interest rates, fees, contract terms, onboarding friction, and integration time. Every product becomes a bundle of parameters.

Taken to an extreme, one could imagine a world where an agent might even assess a bank’s underlying financials (in addition to rate and other terms) to decide on an optimal checking account.

All of this pushes financial providers into a different model. They are no longer marketing to users. In a sense, there are no more “customers,” only intelligent and informed selections – and re-selections – happening in real time.

Second-Order Effects: Markets Everywhere

If financial products are commodities selected by agents, and if agents are optimizing for cost, speed, and reliability, then price becomes the central axis of competition.

This has a predictable effect. Commoditized products + real-time selection = dynamic pricing pressure. Every financial product becomes a market. Mortgages get priced and refinanced in real-time. Insurance gets repriced based on real-time risk models. Consumers and businesses automatically move between deposit accounts to capture optimal yield.

But the shift isn’t just toward automation. It’s toward financial services behaving like tradable primitives. Products are quoted, competed for, and repriced continuously. Providers bid for inclusion in flows that they may only hold for a short time before being displaced.

It’s similar to what’s already happened in public markets – high-frequency trading, order routing, yield aggregation – but extended to the consumer layer. The entire stack becomes price-sensitive and latency-aware.

This introduces real operational pressure. Most financial firms and products aren’t built to reprice every few seconds. They aren’t built to expose real-time availability or cost structure through APIs. But in an agent-mediated world, real-time pricing becomes table stakes.

Regulators, too, will be forced to adapt. Disclosure frameworks assume a human reader, and consent processes assume intention and attention. But what happens when the user delegates those steps to a system? Who’s responsible when something goes wrong – the institution, the agent, or the user who opted in?

If selection is handled by agent platforms, those platforms become the new distributors. Search engines and app stores used to be the gatekeepers. Next, it may be AI agents.

And then there’s the opportunity: if every transaction is a market, someone will build the infrastructure to manage, route, and index those markets. Not the financial products themselves – but the systems that choose between them. That layer may prove to be the most valuable.

Fintech as a Low-Latency Market

The history of financial innovation is the history of distribution. From Visa to Stripe, the best fintech companies have aligned themselves with the prevailing distribution interfaces of their time; they didn’t build new financial products but better ways to reach the user.

AI changes that equation, because it removes the “moat” of distribution. Users no longer choose – they delegate. Financial products are no longer marketed. They are selected based on inputs that are easy to compare and difficult to differentiate.

That makes financial services behave like a continuous auction. Every product becomes a quote. Every user action becomes a bid request. Every transaction becomes an opportunity for someone else to compete and undercut.

Financial providers will be forced to operate at lower margins, with higher transparency, and with infrastructure built for constant repricing. In the end, it’s not just that financial services become commodities. It’s that commodities become markets. Fast, low-latency, always-on markets – driven by agents, cleared by APIs, and priced by algorithms.